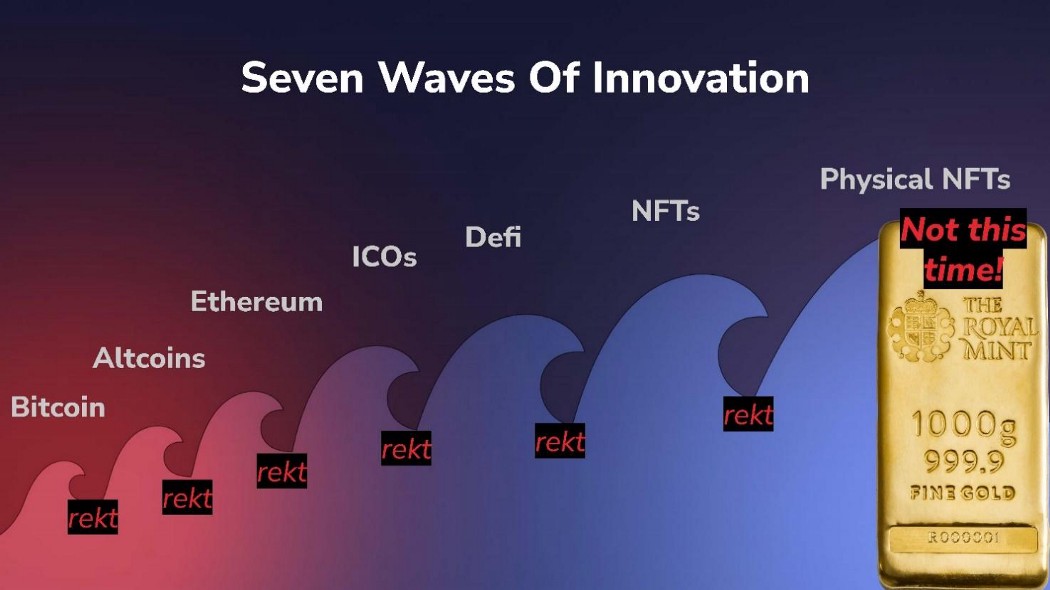

What I’m here to talk about is literally where’s the money. Here we are, we’re now 15 years into crypto, seven or eight years into Ethereum… There’s been an enormous amount of high fortunes made, fortunes lost, made, lost, made, lost, made, lost, made, lost, made, lost, made, lost…

And we could do a lot better, right? Getting out of this cycle of hype and destruction and hype and destruction and hype and destruction, and another bunch of awful, hideous, nonsense happens and a whole bunch of people go… We’ve seen this, and it seems to be never-ending, because it just turns out that deregulated finance is not really safe at any speed. It doesn’t mean it couldn’t be made to work, but we don’t have mechanisms, and as a result we’re stuck in this hell of cyclical boom and blowout. And that hell of cyclical boom and blowout, we have to escape that, if we’re going to turn this into a real industry, rather than something which is going to be like the butt TV show jokes in 20 years, like Friends.

We have an amazing transactional machinery, we can buy and sell anything on the blockchain

To escape this cyclical boom-bust cycle, we have to put fundamentally valuable assets in. We have an amazing transactional machinery, we can buy and sell anything on the blockchain, as long as it can be defined using some kind of digital record, and I mean anything. Things that you didn’t even think were property became property: pictures of imaginary moneys, publicly-tradable essentially stock in companies that only just began to exist, like you do an IPO off your original deck. Lots and lots and lots of things have been tried, where we’ve invented new classes of property, and then we’ve sold those new classes of property on chain.

What I want to suggest is that the flaws of the blockchain industry are the flaws of the new classes of property that we’re trading, not flaws of the technology for trade. We have exchange infrastructure which is powerful enough to do anything, you can imagine a new asset class, you can turn it into a token, you can sell the tokens and the exchange infrastructure can carry it, but the problem is that most of these newly-invented kinds of property are crap. And as a result, you get a wave of enthusiasm where everybody is like “Oh, this new kind of property is amazing!” and then the new kind of property just implodes.

Separate out the fantastic technology we have for doing trade from the crappy assets which turn out to explode

What I’m suggesting is that at a strategic level we can separate out the fantastic technology we have for doing trade from the crappy assets which turn out to explode every time we look at them wrong. And hard assets like gold, real estate, other kinds of commercial assets loaded into the blockchain, with the existing transaction architectures that we have, I believe this is the future of the crypto industry, it’s the everything exchange. And all of the infrastructure that we’ve built, whether the stuff is non-fungible or fungible, whether it’s physical, atomic things, or whether it’s liquid assets like wheat or corn or whatever it happens to be… We have a global exchange infrastructure that’s capable of handling it, we have ways of minting the things, creating and managing them… We could build extremely transparent representations of value, where you can drill down digitally to see every last detail about something, and if this is what we do in the next round of activity in the crypto industry, that round might be the round that doesn’t bust. Because the collapse in these systems has not been a collapse triggered by the exchange infrastructure failing; it’s a collapse that’s been triggered by the assets failing.

Now, I note here FTX is kind of an exception to that. But generally speaking, apart from poorly, poorly-managed financial architectures like Bear Stearns… It’s not that the underlying machinery goes wrong and the Bitcoin blockchain falls over and everybody loses their Bitcoin. The machines for moving the value are secure; the actual sources of value are less secure. If we put more secure, harder value on chain, we’re going to get a very different world, we’re going to get a better world.

There is a report about this stuff that just came out from Boston Consulting Group, and the report is startling — we’re right in the middle of this space, and we’ve found this report remarkably startling! They’re talking about 10% of global GDP, $16 trillion a year of tokenised legal assets by 2030. And they’re not the only people talking in this direction, there’s a whole bunch of other sources that are making noises in this direction. There seems to be a general consensus that hard assets are what comes next, and that consensus is from real-world entities like Deutsche Bank, JP Morgan, like actual players in the real world say tokenisation of equity, security tokens, bond markets, equity and real estate… all of these kinds of things are what they see as being the future of this space.

They’re talking about 10% of global GDP, $16 trillion a year of tokenised legal assets by 2030

And these numbers get much larger than the entire crypto industry very, very quickly. Because we’re not creating that value from scratch, as Bitcoin goes from being worth 25 cents to $25,000; what we’re talking about is taking existing value, and just moving how that value is transferred. Instead of it being transferred on Crest, they’re transferring it on Ethereum — simple.

And this kind of growth, it’s predictable inasmuch as if you have better exchange technology, when people have to sell something or buy something, they will do it using whatever the best available exchange is; if the best available exchange for buying and selling something is a crypto exchange, a crypto exchange is where you’re buying and selling. But at this point, if what you are looking at was a bunch of hard assets — like gold, classic cars, oil paintings, 50 tonnes of wheat, 35 acres of agricultural land — if all of those things are trading in the same exchange as some Bitcoin and some Ether, is that crypto exchange, or is that just the everything exchange?

He’s going to use the blockchain to handle property rights on Mars

As long as you can figure out how to tokenise the value, then you can buy and sell in the same exchange infrastructure we have, using the blockchain to keep the systems honest. And that doesn’t have to stay within this tokenised business-as-usual sector. It is possible to go from tokenised business-as-usual, this set of assets here: listed equity, unlisted equity, other equity, investment funds, bonds, all this stuff… Yes, you can tokenise all of that stuff, you can securitise it, you can have securities exchanges and it will work. But also, there’s other tokenisable assets, which we’ve got $4.8 trillion by 2030… That doesn’t have to be existing classes of assets, that can be new kinds of things. Securitisations of revenue streams, there’s a bunch of that stuff happening in crypto, it’s not so much done in the real world — that could become a large sector. Elon Musk expects to have rockets on Mars by that time, you know that he’s going to use the blockchain to handle property rights on Mars in all probability, because if you’re going to take a new planet and carve it up into acres that people could go out and put solar panels on, probably an actual thing to do would be to use a blockchain, in the same way if you did it in the 1990s you’d use an SQL database.

So, this prospect of taking the existing systems and getting them on chain, and taking the new systems and getting them on chain, you wind up in a position where everything becomes interfungible, rather than having a bunch of separated, balkanised markets, which are very, very loosely connected. This also opens up possibilities for things like smart barter. There’s a company called NeoSwap, they have an algorithm for switching around value between lots of different people, as long as everything is represented as NFTs, without requiring it to be bought and sold at every step — extremely powerful, because it means you can do trade with minimum liquidity.

And it’s not an unrealistic rate of growth, when they say $16 trillion by 2030. If you look at the influx of stablecoins, $160 billion of hard assets went into the crypto ecosystem in a two-year period, and the rapidity of that transfer was because you didn’t have to make the assets from scratch; the assets were already there, you just move them out of the wire transfer land and you put them back into blockchain land. So, if you were doing this kind of transfer, but it was stocks, it was bonds, it was real estate, it was gold bullion, it was everything else, you could get a very, very rapid movement of trillions of value on chain, without having this weird thing that money is being printed and coming from nowhere — it’s not a fiat economy at this point; it’s actually an asset-backed economy.

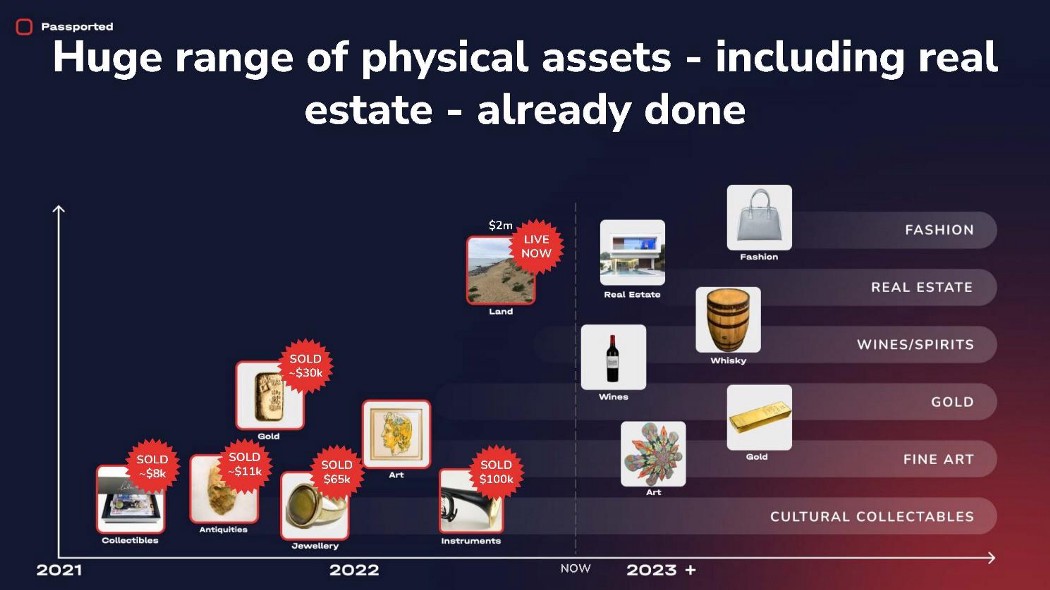

Now, the question then is could this possibly work, is it legally possible to do this? And the answer is yes. My company has done this in custodied assets in five jurisdictions, and transactions in another three, out of the 170 jurisdictions that it’s possible to do this in. So this is not some kind of long-term, long-reach pipedream; buying and selling physical assets as tokens with the correct legal bindings behind them is a thing you can do here and now over almost the entire world. It’s trickier if the things that you’re buying and selling are things like securities, but if you’re selling commodities, or if you’re selling gold bricks or whatever it is, physical artwork, classic cars… The vast majority of the sort of battle rattle of civilisation is saleable right now all over the world, on relatively clear and easily understood deterministic legals. It’s not that we need massive changes in law in every jurisdiction to be able to do this; buying and selling a physical object on eBay and buying and selling a physical object on OpenSea look very similar to the law.

And that track record, we’ve literally just gone in the last year and a half, asset class by asset class by asset class by asset class, starting with the infamous William Shatner toy collection — I say “toys”, but I think that’s a bad word for that stuff; memorabilia [laughter] Yeah, because one does not want to invoke the wrath of Shatner — just look what he did to Jeff Bezos! That landscape, we’ve just gone asset class by asset class by asset class by asset class, making sure that it works… And in the course of a year and a half, we literally went from Shatner’s memorabilia collection to a two-million-dollar plot of land on the south coast of England. And that trajectory is not just stuff inside of the UK; that’s across a whole bunch of different countries.

We went a little deeper into the legals, we solved it for a whole set of jurisdictions and a whole bunch of different asset classes

So, that capability, now that it’s here, we can scale assets on this platform very, very fast. And we are not the only people doing this. We took a somewhat different approach from most of the other companies who are in this space. Most of those companies operate inside of one jurisdiction for one asset class; we went a little deeper into the legals, we solved it for a whole set of jurisdictions and a whole bunch of different asset classes. But at the end of the day, it’s not just “Hey, Mattereum does this amazing thing!” it’s that this amazing thing is the future of the blockchain space, a whole bunch of different people have understood that… And what does this space look like in two years, if you come to conferences like this, and two-thirds of the room are gold industry, real estate industry, airline industry, talking about tokenising and selling the physical things that they’re buying and selling: airline tickets, concert tickets, real estate… I keep coming back to bullion, because given how unstable the financial markets are and how much inflation we have, bullion is a potentially very important asset class, once you can make it appropriately tradable internationally in blockchain-style transactions, rather than the current restrictions which make it hard to make payments in gold.

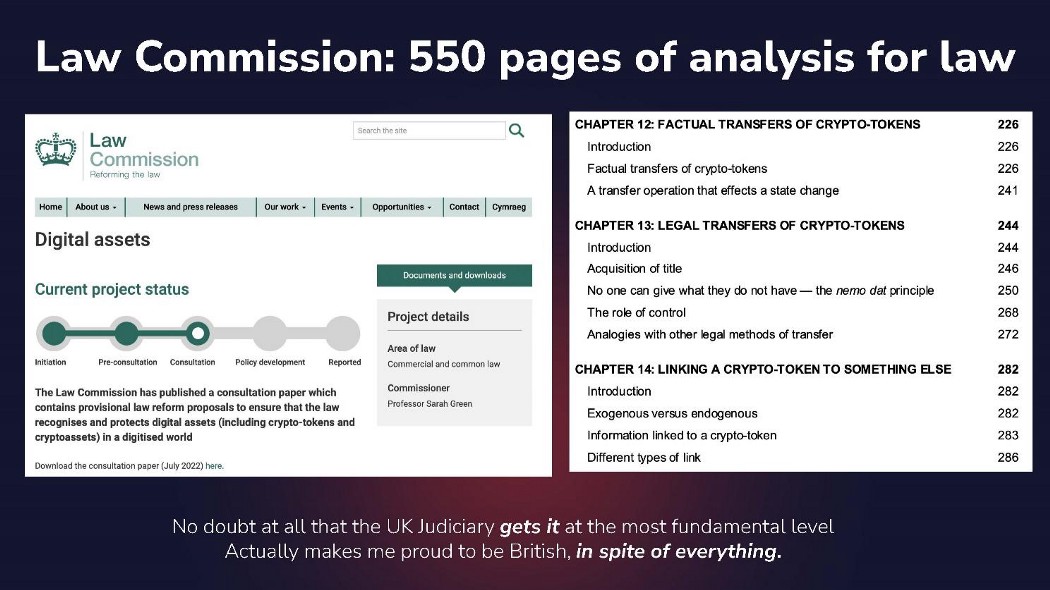

The reason that we can do all of this stuff is British law is really, really substantial on these kind of issues. The legal innovation that’s happened in the UK in the last five years, in terms of really getting down to the bones of what the blockchain is, what blockchain transactions are, what tokens are, how all of this stuff really works is absolutely world-class — I mean, this stuff is profound!

Everything is being seen as a financial instrument. This Law Commission document will change that

The Law Commission has a consultation document, it’s a philosophical examination of what digital is. Very sophisticated legal minds looking at digital, and saying, “From first principles, under English common law, what is that really?” And the advantage that it has for us as the industry is that right now the sort of power grab is that everything is being seen as a financial instrument. This Law Commission document will change that. If something is regulated as being a toy, then if it’s a digital toy or a physical toy, it’s still a toy, and English common law says, “This is how you handle toys, and here’s the digital part, and here’s the non-digital part of the law.”

So, in breaking down this idea that everything on chain is a financial asset, it also hugely reduces the complexity of doing ordinary, everyday things on chain. Because if you’re a corner shop that makes NFTs, you really shouldn’t be regulated in the same way as a bank. You’re an artist, you’re a working artist, you have a loft, you paint things paintings, you take pictures and you sell the pictures… If I sell them on eBay I don’t need any kind of license, and if I sell them as an NFT… You know, it’s just the regulation is kind of out of whack, and the reason the regulation is out of whack is because it wasn’t a regulatory problem, it’s a legislative problem, and the UK Judiciary are going through the process of figuring out the correct legal treatment of these things.

And if you compare this approach to how primitive the approach is in for example America, this is kind of sort of what Britain does for a living. We’re really good at this kind of deep problem-solving in a lot of different domains, this one happens to be legal, but don’t forget the the AI revolution also started in the UK with DeepMind. So, this is the sort of fundamental bedrock.

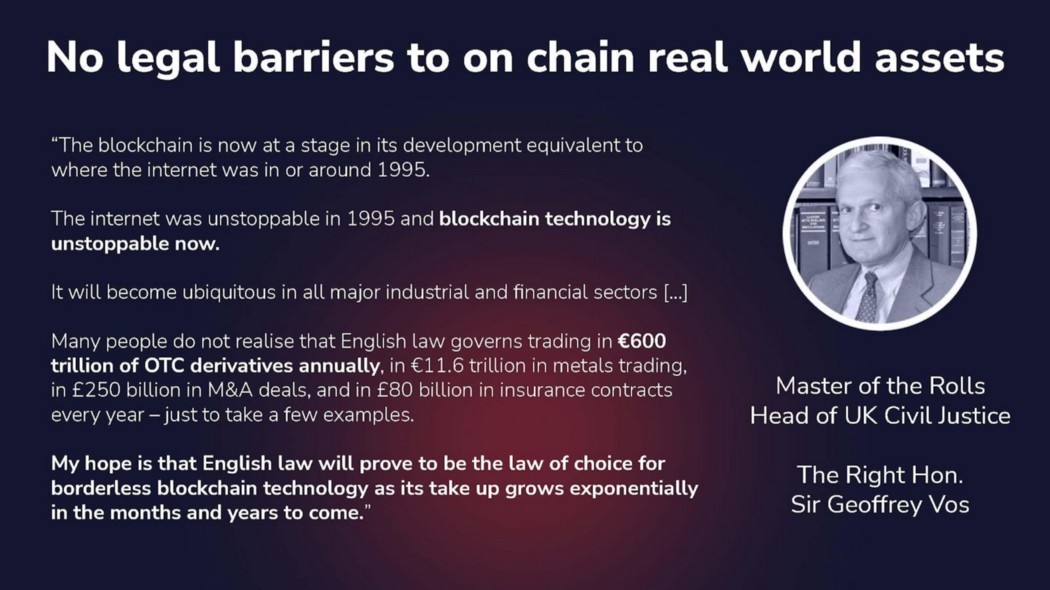

And then in the UK, this guy here, Sir Geoffrey Vos, is the most senior civil judge in the UK, so he’s the boss of all bosses for anything commercial… This is his statement on the blockchain, delivered I think February of this year, and the real payload is this section at the bottom: “My hope is that English common law will prove to be the law of choice for borderless blockchain technology, as its uptake grows exponentially in the months and years to come,” drawing parallels to the €600 trillion of OTC derivatives that currently run under English law. And those derivatives are from all over the world, but because you can transfer the seat of dispute, so you could pick your choice of courts and judges, everybody that can bring their disputes into English common law does, because our system of justice is kind of fantastic. I mean, yes, it’s still lawyers, and yes, it’s still hard, but it’s dramatically less hard, because there’s so much sophistication in the legal system — no offence to our cousins over there; he’s giving me the look, the stern eye… [laughter] “Yeah, yeah.”

“My hope is that English common law will prove to be the law of choice for borderless blockchain technology, as its uptake grows exponentially in the months and years to come,” — Sir Geoffrey Vos

Nonetheless, we have high-level support, there’s no doubt at all that this as an approach is credible, and the expectation is that English law is going to become better and better and better at handling digital assets in a way that is not upsetting. As a result, if you bring your digital assets to the UK so they’re all handled under UK law, you don’t wind up with this terrible problem where the local jurisdiction that you’re in doesn’t understand how to handle the assets, and you wind up regulating 120 countries, which is not going to work. We need a uniform framework, and if it’s good enough for the derivatives market, it ought to be good enough for digital.

Comment: I want to actually add, I was thinking while you were saying that: one of the things you cannot do in the United States is you cannot by contract grant a court jurisdiction, so we can’t enter into a contract where I say courts in Kansas or in New York will adjudicate a dispute, if there’s no nexus to that jurisdiction. That’s actually not a problem here. Anybody, somebody in Singapore can enter into a contract with somebody in Russia, saying that disputes will be adjudicated in London, and English courts will accept that jurisdiction is my understanding — it’s a very different approach, and it’s smart.

Good law lets you get physical assets on chain.

Yeah, yeah. And particularly if you’re working with arbitration courts, LCIA arbitration… You get multiple different mechanisms for picking your venue, you get access to good law, and the good law lets you get physical assets on chain.

Final slide: this is a map of what I think are the eight fundamental sources of value on the blockchain. Just about anybody that is making money on chain is executing one or more of these strategies, and a lot of the confusion and the damage that we’ve seen on chain comes because people believe that somebody is executing one strategy, and they’re actually executing another strategy.

The big problem that we have on chain is that you’ve got people who you think are selling transactional efficiency, and they are actually Ponzi schemes! And that confusion about what you’re doing for a living, what the business that you’re in, this is the thing that has brought the blockchain into such terrible disrepute, because the system is so powerful that you can turn almost anything into a Ponzi scheme without it being apparent!

If we’re going to save the industry, we have to get away from the bad sources of value generation, and only be in the good ones.

So, my recommendation is: for the next phase of the blockchain, make absolutely sure you understand what business your counterparties are in at every single step. And for yourselves, look at this very hard, and make sure that you’re somewhere up here with transactional efficiency, or you’re an exchange, or you’re selling something that you made yourself, and that you’ve not drifted into one of the dead zones on this thing. Because if we’re going to save the industry, we have to get away from the bad sources of value generation, and only be in the good ones.

Postscript

Crypto’s seven waves of innovation have each mimicked a Perez Surge Cycle (here’s a highly recommended piece from 2019 on blockchains and the surge cycle). In 2019 we were not at the Perez Turning Point, because there was not enough infrastructure built to be rolled over into new successful companies. In 2019 we had the bubble burst, but it was replaced by another bubble, not by the Synergy and Maturity phases of the technological deployment cycle.

At the Perez Turning Point a huge bubble bursts. People say “never again.” It seems like the entire space is crumbling and a lot of assets are sold off for peanuts to people that actually know how to run companies. Regulation comes in to protect investors from another round of the bubble, and the space becomes mainstream, boring, and yes — highly economically productive.

It’s happened in sector after sector over decades and generations and now its our turn.

To contact Mattereum https://mattereum.com/contact-us/

All Comments