— A Deep Dive into the True Cost of AI: From TCO Complexity to the AI Credits Economy

Enterprise spending on Generative AI is spiraling out of control at a visible pace. In 2025, this figure reached approximately $37 billion, representing 3.2× growth compared with the previous year. During the same period, total venture capital investment in the AI sector reached approximately $211 billion, an 85% year-over-year increase, setting a new historical record. Capital is flooding into the space, yet very few enterprises can clearly answer one of the most fundamental questions:

How much is one Token actually worth? How should we truly purchase “intelligence”?

As a platform processing massive-scale model interactions and AI Credits settlement every day, UniKey Research Institute has compiled the industry data, cost models, and real-world consumption structures observed over the past six months into this research report.

Breaking it down, we arrive at five key conclusions:

First, there is an entire industrial gap between the accounting price of Tokens and their true cost. The real cost must be calculated through Total Cost of Ownership (TCO) rather than simply relying on the unit prices displayed on API invoices.

Second, Token pricing is undergoing a “two-way divergence”: “Intuitive Tokens” designed for simple tasks are rapidly becoming cheaper, approaching marginal cost levels, while “Reasoning Tokens” responsible for complex inference continue to maintain a long-term premium valuation.

Third, the traditional binary choice of “building self-owned servers vs. renting APIs” has developed three critical blind spots in the Agent era, causing both approaches to gradually fail in opposite directions.

Fourth, the optimal solution is a third path: introducing an “Intelligent Procurement Layer” between computing resources and business requirements.

Fifth, this is exactly why we created UniKey AI Credits — in the final section of this report, we will openly present our own answer.

I. A Scissors Effect That Is Gradually Opening

To understand the cost of Tokens, we must first understand the capital structure of this industry. On the supply side, technology giants are conducting capital expenditures with unprecedented intensity: acquiring GPUs at massive scale, building data centers around the world, and even extending their reach toward nuclear reactors and space-based data centers, attempting to break through the limits of global energy supply and thermal management. Meanwhile, on the demand side? Revenue is growing, but it is still far behind the slope of investment expansion — the AI industry remains a considerable distance away from overall profitability.

The slow monetization on the market side and the massive investment on the supply side have created a huge scissors gap. Where does this gap ultimately land? It lands on every enterprise decision-maker who follows the AI infrastructure trend, purchases computing power aggressively, yet cannot accurately calculate the real cost.

More dangerously, the Agent era is amplifying this scissors effect. When enterprises delegate business processes to multi-agent systems, Token consumption is no longer a linear consumption model of “one user question, one model response.” Instead, it becomes an internal circulation between Agents, expanding by dozens or even hundreds of times — planning, reflection, retrieval, tool calling, cross-validation, every stage is consuming Tokens.

We define this as the “Token Amplification Effect”: you think you are deploying a single assistant, but in reality, you are hiring a tireless workforce that never gets tired — and never checks the bill.

Therefore, before making any AI transformation decisions, every CXO must first answer the most fundamental question: How much is one Token actually worth?

II. Dissecting a Token: How to Calculate the Real Cost

Token economics provides the answer: do not look at a single invoice; calculate the Total Cost of Ownership (TCO). The formula is approximately:

Depreciation, Torn Apart by the Speed of Iteration. Large-scale AI computing infrastructure is not a traditional IT asset. With extremely rapid technological iteration, the industry has broadly moved away from conventional 5-year depreciation cycles and shifted toward aggressive 2–3 year depreciation models. More importantly, there is the “computing capacity tidal effect”: business workloads have daytime peaks and nighttime valleys, but depreciation never sleeps — for clusters operating at only 50%–60% utilization, the depreciation cost allocated to each effective Token can deteriorate exponentially. Put simply, you are paying for 24 hours of depreciation, but only utilizing 12 hours of actual capacity.

Electricity Costs Are a Double Tax. The essence of Token production is transforming every watt of electricity in the carbon-based world into Tokens in the silicon-based world. This refinement process comes with a double tax: beyond the direct inference power consumption, there is also the penalty from Data Center PUE (Power Usage Effectiveness) — for every unit of electricity consumed for computation, an additional portion must be paid for cooling, along with expensive cluster interconnect and bandwidth transmission costs.

There is also an invisible “hidden engineering tax” that never appears on the invoice: the cost of frequently calling vector databases and enterprise knowledge retrieval systems (RAG) to reduce model hallucinations; compliance guardrails that every output must pass through — including sensitive content filtering, security audit models, and audit archiving; as well as the personnel and tooling costs associated with operations engineers, security infrastructure, and monitoring systems.

The cost structure of large models has never been a pure software game. Instead, it represents a new industrial-scale marathon where energy efficiency, chip architecture, and fixed asset turnover rates all play critical roles.

III. The Two-Way Price Divergence: Deflationary Intuition, Expensive Reasoning

If Token costs were simply “expensive,” the problem would actually be much easier. The real complexity lies in the fact that different types of Tokens are moving toward two completely opposite pricing directions.

Borrowing the framework from Thinking, Fast and Slow, model outputs can be divided into System 1-style “Intuitive Tokens” and System 2-style “Reasoning Tokens.”

Intuitive Tokens are experiencing aggressive technological deflation. On the hardware side, process upgrades, increased transistor density, and architecture optimization are dramatically increasing output per unit of power consumption; on the software side, Mixture-of-Experts (MoE) models activate only a portion of parameters for each inference, while quantization technologies (FP16 → FP8 → FP4) continuously reduce memory requirements by half. Tracking data from the Stanford AI Index shows that the inference cost of GPT-3.5-level models has dropped by more than 280× in less than two years — falling from $20 per million Tokens to $0.07, and the decline curve continues to steepen after entering 2026. Market validation shows that in July 2026, next-generation mainstream models have already entered the market with limited-time pricing as low as $2 per million input Tokens. The price of Intuitive Tokens is rapidly approaching the physical marginal cost composed of electricity and depreciation.

Reasoning Tokens, by contrast, will maintain long-term premiums. Complex reasoning, multi-step planning, code architecture, and research-grade analysis generated through massive inference-time compute, deep logical self-play, and extended reasoning processes will continue to carry significant premiums, becoming the true core value of paid AI services.

An interesting supporting example comes from the routing platform OpenRouter: over the past year, the Token share of the three major U.S. AI providers (Google, OpenAI, Anthropic) on the platform declined from approximately 70% to around 30%, while Chinese open-source models occupied six positions among the top ten models listed (Bloomberg / OpenRouter). It should be noted that this data contains sample bias — users of aggregation routing platforms naturally favor lower-cost open-source models. However, the same dataset also reveals that while leading closed-source providers have experienced a significant decline in Token share, they continue to capture far higher revenue than their share through premium pricing. The battlefield of volume belongs to deflationary Intuitive Models, while the battlefield of revenue belongs to premium Reasoning Models — this two-way divergence is being simultaneously validated on the same platform.

This divergence means that “buying intelligence” is no longer about purchasing a single product, but about constructing a portfolio across a pricing spectrum — customer service conversations use near-zero-cost Intuitive Tokens, investment research reports use high-priced Reasoning Tokens, image and video generation rely on specialized multimodal models, and coding tasks utilize programming-optimized models.

The question then becomes: when the optimal procurement strategy is “dynamic multi-model orchestration,” does a self-built solution that places all its resources on a single model still make sense?

IV. The Classic Divide Is Beginning to Fail

There has always been a classic breakeven line between “direct closed-source API procurement” and “private deployment”: an average daily actual consumption of approximately 50 million Tokens (corresponding to an annual TCO of around 900,000 RMB).

The calculation logic is roughly as follows: a high-performance GPU delivers an actual inference throughput of approximately 100–150 Tokens per second. An 8-GPU configuration provides a combined throughput of around 1,000 Tokens per second, with a theoretical maximum daily production capacity of 86.4 million Tokens at full utilization. Based on a commercially healthy utilization rate of 50%–60%, the optimal daily output limit of an 8-GPU inference server is approximately 50 million Tokens per day. At an industry average price of around 50 RMB per million Tokens, the annual API expenditure for a daily consumption of 50 million Tokens is approximately 912,500 RMB; meanwhile, the annual fixed TCO of building equivalent capacity in-house (depreciation + hosting electricity costs + hidden engineering tax and personnel costs) is approximately 900,000 RMB — 912,500 RMB vs. 900,000 RMB, which represents the financial tipping point between renting and building.

It should be noted that this breakeven point is highly sensitive to the assumption of a “50 RMB per million Token” pricing level — and the previous section has already demonstrated that Token prices are undergoing rapid deflation. Every downward adjustment in API pricing shifts the rental cost curve downward, while simultaneously pushing the breakeven point for private deployment higher. In other words, this divide is not a fixed line, but a line that is continuously moving away from self-built infrastructure.

Even without considering price changes, when this framework is placed into the real enterprise environment of 2026, it still contains three increasingly significant blind spots.

Blind Spot One: It assumes workload follows a straight line. Real business demand is tidal: consumption can surge tenfold during campaign periods and fall back to the bottom during off-seasons. Private deployment faces queue collapse during peaks (latency spikes and user experience degradation), while during valleys it continues paying idle depreciation costs (extremely low asset utilization efficiency). The “certainty” purchased through fixed TCO becomes a dual penalty under fluctuating workloads.

Blind Spot Two: It assumes you only need one model. Private deployment locks you into the capacity of a single model, while optimal procurement has already evolved into a multi-model combination — and the optimal solution changes every quarter. Supply-side risks are also becoming more realistic: in June 2026, a leading closed-source AI service experienced a full-scale outage lasting several hours, causing global automation workflows dependent on a single API to collectively stop; during the same month, one of the most powerful flagship models was taken offline for nearly three weeks due to U.S. export control directives. Single-provider dependency means placing business continuity in someone else’s data center and under another country’s policy environment.

Blind Spot Three: It does not price for the Agent era. Under the Token Amplification Effect, consumption is no longer determined by “number of employees × usage frequency,” but by “number of Agents × task complexity × depth of internal loops.” In June 2026, leading AI providers had already announced the abandonment of “unlimited” subscription pricing for Agent products and shifted toward usage-based pricing. When even sellers can no longer sustain unlimited subscription models, buyers continuing to make heavy-asset decisions based on “forecasted capacity” is no different from trying to carve a boat to mark where a sword fell into the water.

“Self-build vs. Rent API” is a question from the previous era. The real question of this era is: who will provide enterprises with intelligent measurement, routing, and settlement?

V. The Third Path: Intelligence Procurement Layer

We define this layer as the Intelligence Procurement Layer: positioned between enterprises and global computing resources, it connects to multi-model supply on the infrastructure side, while transforming “intelligence” into a manageable business resource that can be budgeted, audited, and allocated.

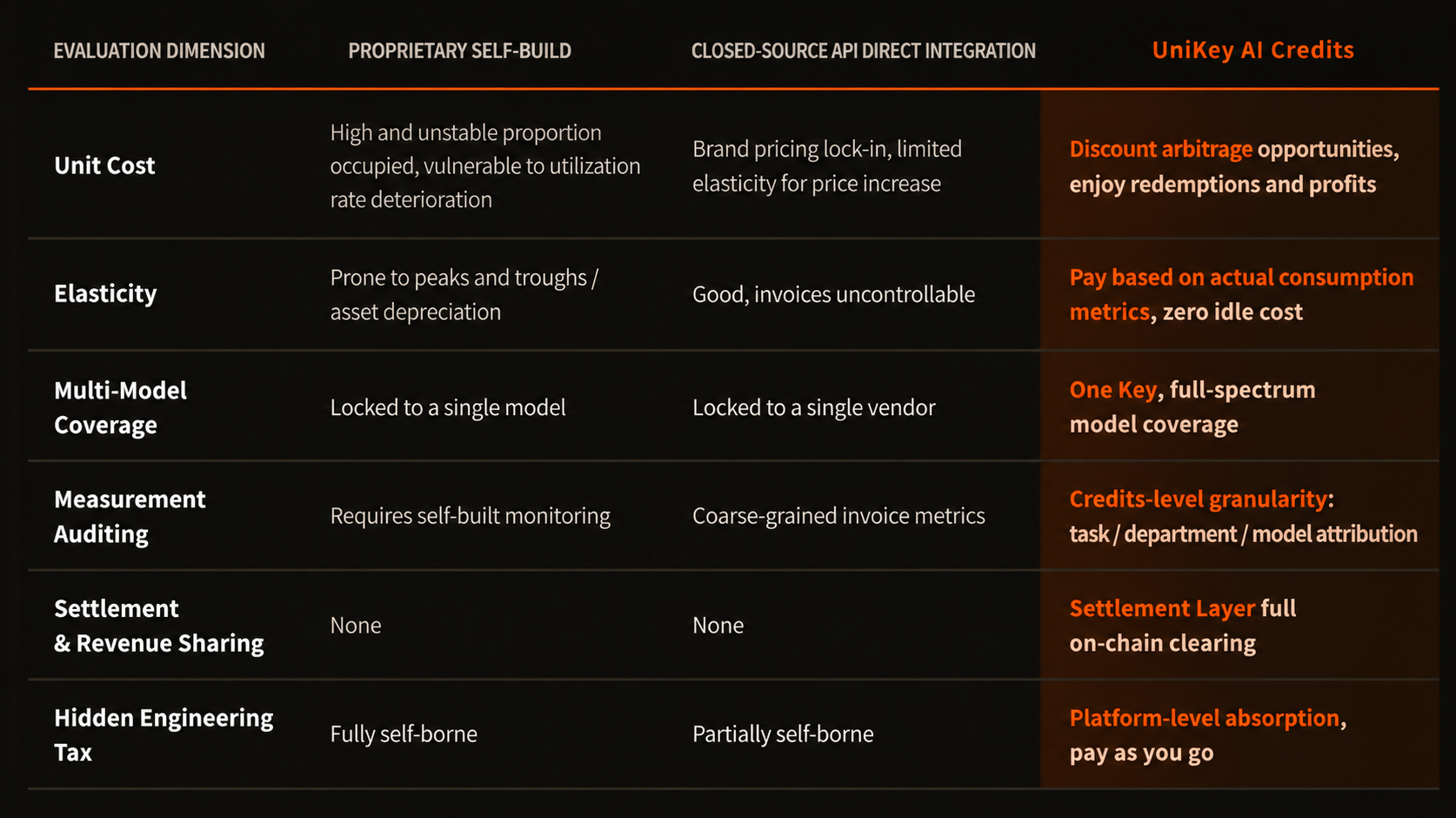

To evaluate any potential solution, five dimensions should be considered:

1. Unit Cost — Can it capture the benefits of technological deflation and channel pricing opportunities, keeping the actual cost per million Tokens consistently below direct procurement pricing?

2. Elasticity — When consumption surges tenfold, can it avoid queues? When demand falls back to the bottom, can it avoid depreciation costs? Can it truly achieve payment based on actual consumption?

3. Multi-Model Coverage — Can a single access layer connect to the optimal models across the full spectrum of text, image, video, code, and search capabilities, while automatically switching when a specific model experiences downtime or is removed?

4. Measurement and Auditability — Can every call, every task, and every department’s consumption be precisely accounted for, traceable, and controllable?

5. Settlement and Revenue Sharing — When intelligence usage involves multiple participants (model providers, capability providers, service providers, and channel partners), can value be properly settled and distributed?

Looking back at the two traditional solutions through these five dimensions: self-built infrastructure only barely passes under conditions of extremely large and stable demand, while losing points across almost every other dimension; closed-source direct procurement performs relatively well in terms of elasticity, but remains constrained by listed pricing, single-provider dependency, and coarse-grained billing, while settlement and revenue sharing capabilities are almost entirely absent.

The market needs an answer with all five dimensions fully activated.And this is exactly what we are building.

VI. Our Answer: UniKey AI Credits, Transforming Token Procurement into Intelligent Employment

Frankly speaking, all the research discussed in the previous five sections ultimately points back to the product design of UniKey itself. We do not avoid this fact — it is precisely because we process real-world AI calls, consumption, and settlements every day that we understand better than anyone how difficult it is to satisfy these five dimensions simultaneously. The concept of UniKey AI Credits can be summarized into four points:

Unified Measurement. 1U = 10,000 AI Credits, serving as the official unified denomination. Models, images, videos, APIs, Agents, Skills, Workflows — all consumption is converged into the same measurement unit. Enterprises can monitor intelligent consumption just like reading an electricity meter: which department, which task, and how much was consumed can all be clearly presented in a single bill.

Multi-Model Routing. One Key provides unified access to global models and multimodal capabilities: Intuitive tasks are automatically routed to low-cost models benefiting from ongoing deflation, while Reasoning tasks are directed to premium flagship models; when any provider experiences downtime or is removed due to policy changes, traffic is automatically switched. Enterprises no longer need to bet on any single model — it is equivalent to holding an “index fund of global intelligence.”

Price Opportunities. Returning to the previous breakeven point of 912,500 RMB vs. 900,000 RMB, UniKey’s channel and incentive ecosystem provides pricing opportunities. With the same annual consumption, the actual bill can be significantly lower than direct procurement pricing — effectively pushing the “rental” cost curve downward once again beyond technological deflation, further weakening the financial justification for self-built infrastructure. (Specific policies are subject to the latest official plans.)

Unified Settlement. When a task is completed through collaboration among multiple Agents and multiple Skills, who contributed what, and who should receive what? The Settlement Layer records every call, execution, delivery, and consumption event, making measurement, allocation, and revenue sharing auditable and traceable — this is also the fundamental difference between an “Intelligence Procurement Layer” and a traditional “API Aggregator.”

Taken together:

Looking back at every revolution of production factors: the widespread adoption of electricity did not rely on larger power generators, but on power grids and electricity meters; the flow of capital did not depend on more gold, but on exchanges and clearing houses. Technological deflation will continue to push the production cost of intelligence toward marginal cost, but the distribution, measurement, and settlement of intelligence will always remain scarce.

Token is the new oil. And we believe: those who define the unit of measurement will ultimately define the price.

This is exactly what UniKey is building.

All Comments