From CoinShares Research Blog by James Butterfill

In the commodities world a demand shock refers to a sudden and significant change in the demand for basic goods or raw materials, triggered by unforeseen events. Positive demand shocks result from increased demand, potentially due to technological innovations, policy changes, or shifts in consumer preferences, driving prices up. The Chinese economic boom at the beginning of the 21st century created a commodities demand shock as property development ramped up, this led to steel prices rising 793% between 2000 and 2008. A combination of weaker economic growth following the great financial crisis, and a supply response in the form of increased production, then led to an 80% fall in steel prices over the following decade.

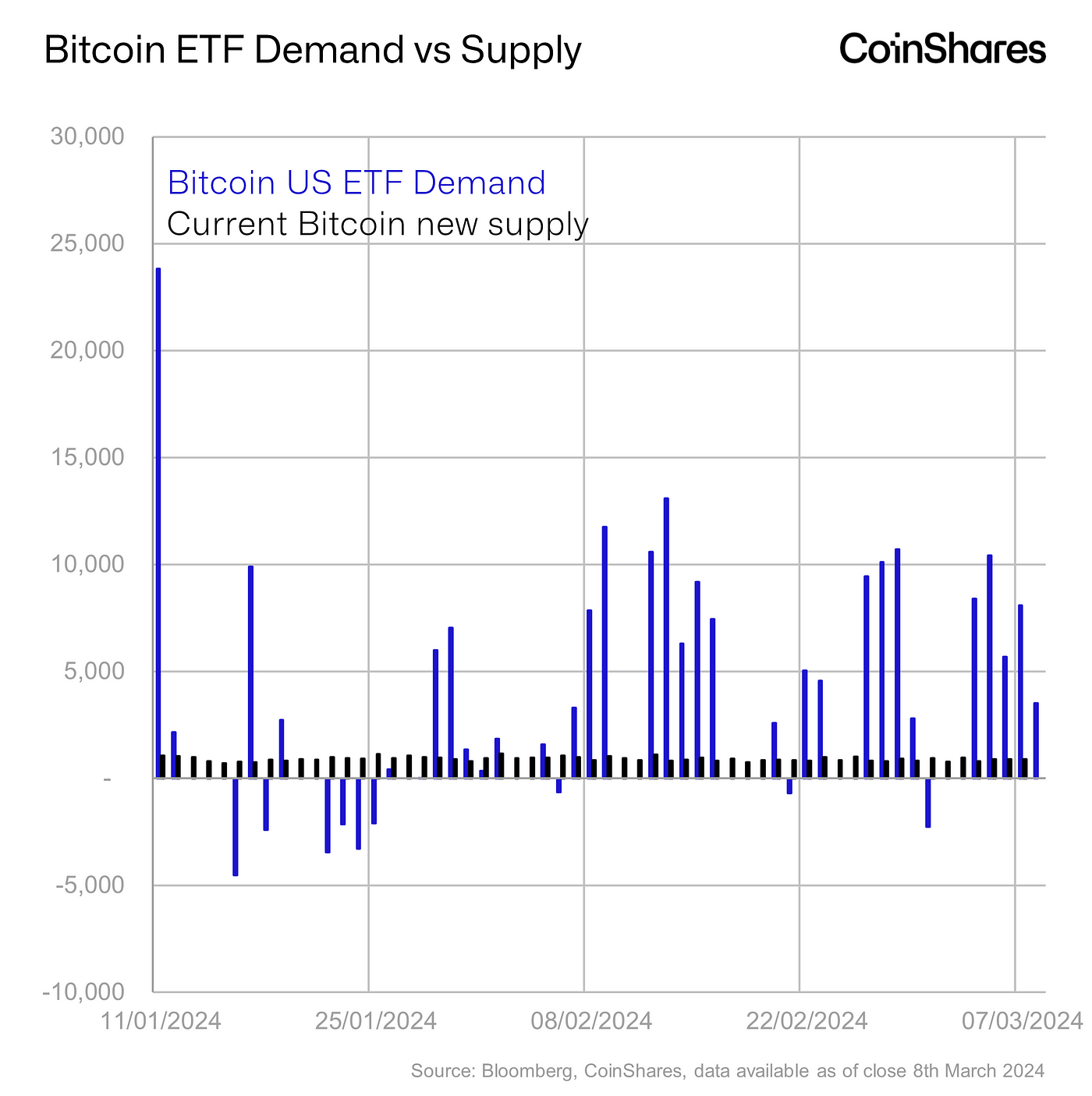

We believe Bitcoin is currently experiencing a positive demand shock. The SEC approval of a spot-based EFT has given access to over US$14 trillion of assets, while this was known, its timing was not and the magnitude of the resulting inflows were not a matter of widespread consensus. So far, the launch of the ETFs on the 11th of January has led to an average daily demand of 4500 bitcoins (trading days only), while only an average of 921 new bitcoin were minted per day.

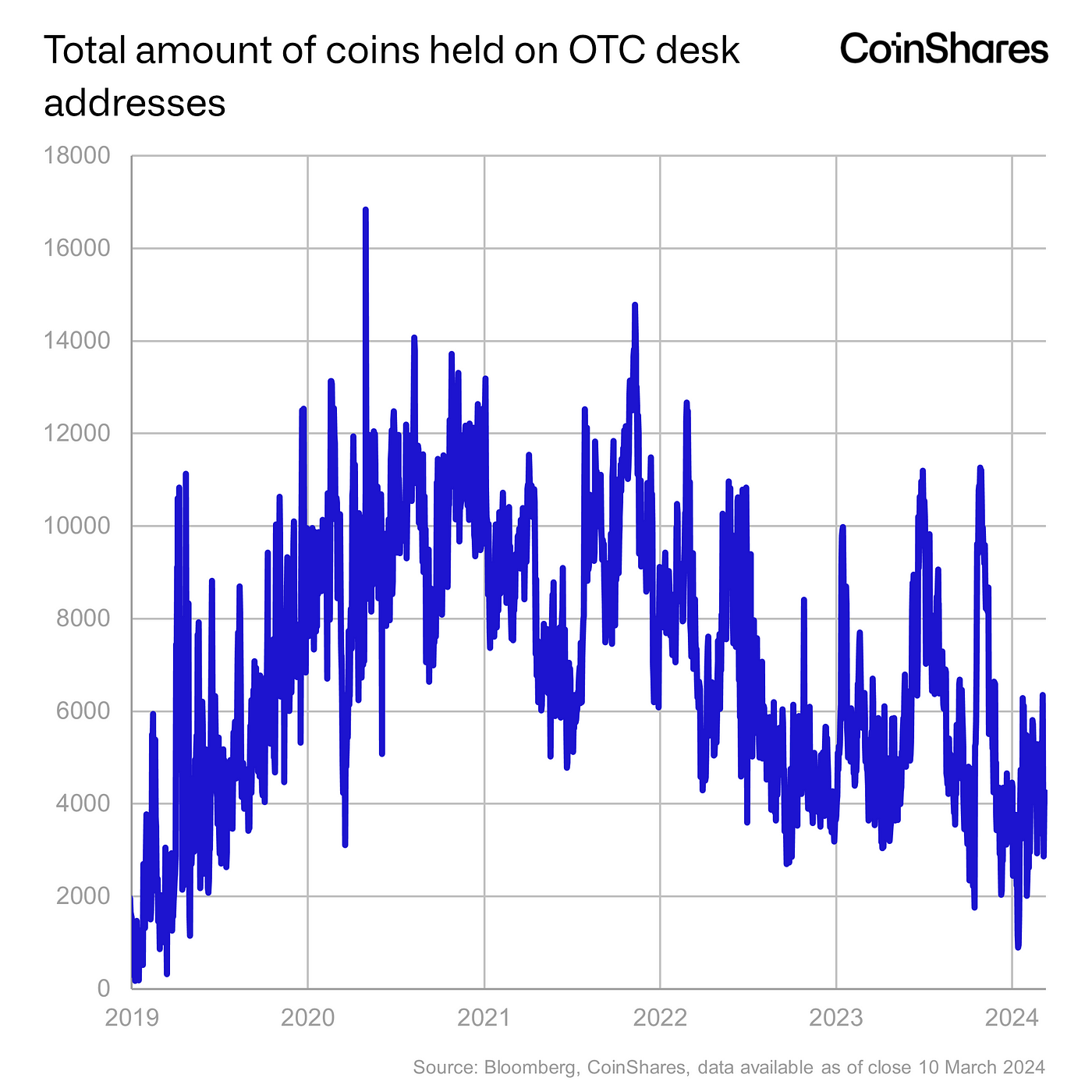

This has led to the dramatic price rises we have seen in recent weeks, as the newly minted supply cannot keep up with demand, leading to ETF issuers having to source mainly from the secondary market. We can see this in the data, where OTC desk coin holdings have fallen by 74% since their 2020 peak, much likely due to ETF demand in recent years.

US ETFs have seen record breaking US$10bn in flows in the first two months, dwarfing the launch of the first Gold ETF by iShares in 2005 of US$288m over its first two months. In the first 2 months of 2020, just prior to the halving, ETPs saw US$436m of inflows representing 11% of total assets under management, remarkably similar to today, where recent inflows also represent 11%, although in nominal terms the inflows today are 23x higher than 2020.

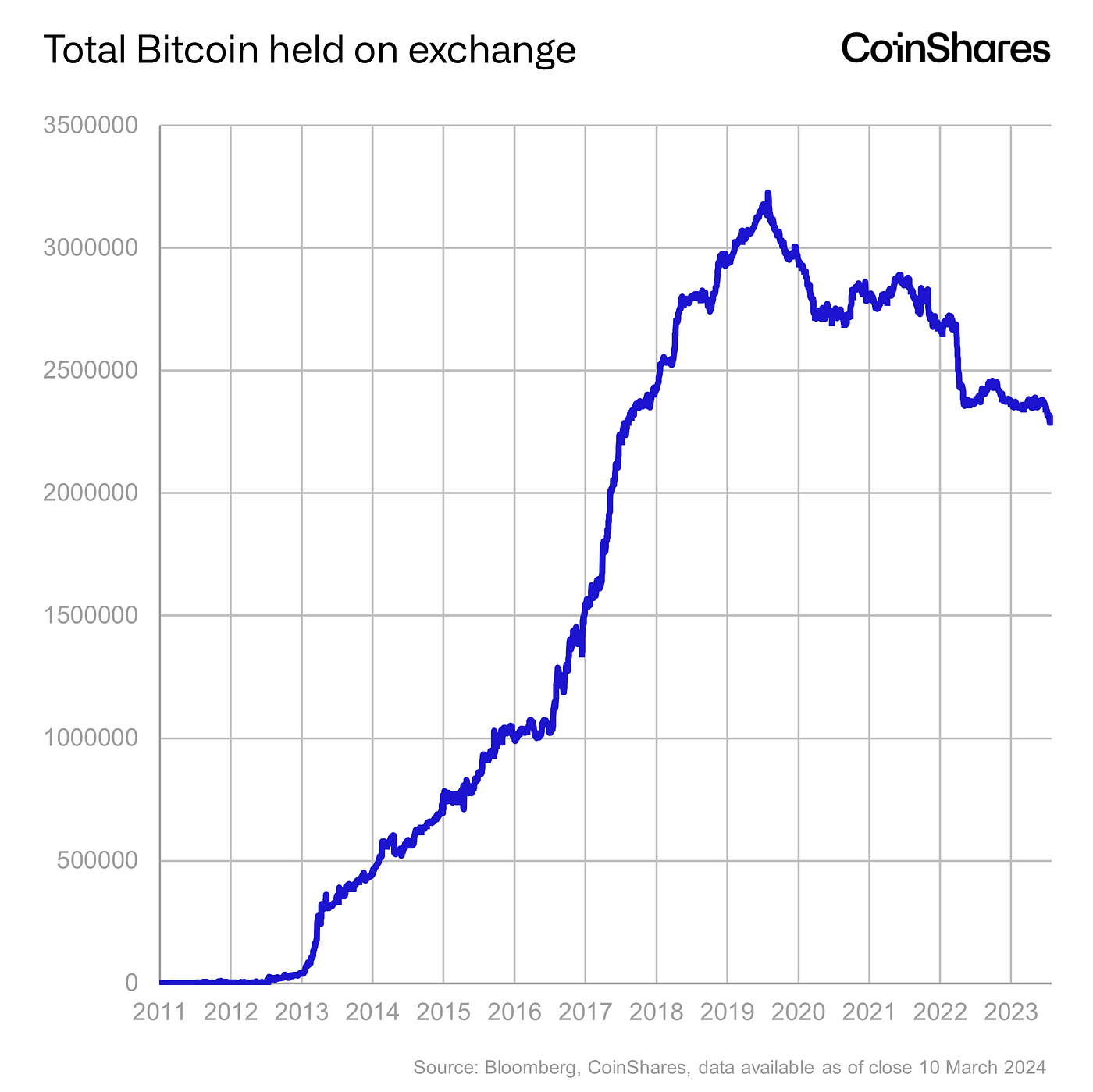

We have also seen a significant reduction in bitcoin held by exchanges, which have fallen 29% since 2020 as investors utilise ETPs more and self-custody their bitcoin as they increasingly see it as a store of value.

At current rates of ~4500 bitcoin a day it would take 573 days to run that exchange balance down to zero — so a long way to go still.

After a demand shock in the commodities market there is typically a supply response. Over time, suppliers adjust their production levels in response to the new demand conditions. In the case of a positive demand shock, producers might increase production capacity or seek ways to enhance efficiency to meet higher demand. However, this is where Bitcoin’s similarities to the commodities market ends, as Bitcoin has a fixed immutable supply, which is programmatically designed to halve the newly issued supply every 210,000 blocks, or roughly every 4 years.

Ultimately, the market seeks a new equilibrium at the intersection of supply and demand. This adjustment process can be swift or slow, depending on the magnitude of the shock, and given Bitcoins supply is inflexible, it is only the price that can seek a new equilibrium. This is why we have seen such dramatic price rises in recent months, with the combination of the ETF launch demand and the upcoming halving exacerbating the issue.

The halving is well-known information and should, in theory at least, already be factored into the price. One could argue that the post-2020 halving price increases were more a result of the US COVID stimulus cheques rather than the halving itself. Statistically there is only a sample size of 3 prior events to go by and so it is dangerous to draw any conclusions — we have written more detail about this here. However, there might be an element of it becoming a self-fulfilling prophecy, particularly if there are a large number of trades linked to the event, although at present futures market trader positioning around the event is low.

Regardless, there are several other price supportive factors for Bitcoin prices this year, among the most significant developments are the platforms in the US that enable Registered Investment Advisors (RIAs) to include Bitcoin ETFs in client portfolios. However, we believe there will eventually be a reduction in these inflows, diminishing their impact on prices. If these flows start decreasing later this year, we anticipate that Bitcoin prices will realign with expectations for interest rates. With the US Federal Reserve expected to lower interest rates later this year, this is likely to materialise as additional price support for Bitcoin.

All Comments