Table of contents

1. Definition and development history of RWA

2. Market size and growth trend

3. RWA Technical Path and Core Standards

4. Typical RWA asset categories and practical applications

(I) Typical RWA asset classes

2. Practical application of RWA

(III) RWA Practical Issuance Process

5. Current status and representative projects of RWA in the global, China, US and Hong Kong markets

VI. Regulatory policies on RWA in various regions

(I) Hong Kong’s regulatory policy: from pilot innovation to dual-track supervision

(II) US regulatory policy: functional testing and judicial precedent-driven

(III) Dubai Regulatory Policy

(IV) Comparative summary of RWA regulatory environment in various regions

VII. Future Prospects and Potential Forecast

introduction

With the rapid development of the global digital economy, RWA transforms traditional assets into digital tokens through blockchain technology, significantly improving the liquidity, transparency and accessibility of assets. This innovation is considered to be a key force in promoting the digital transformation of financial markets. Especially in 2025, with the accelerated influx of institutional funds and the gradual clarification of the regulatory environment, the RWA market is showing a rapid growth trend. This report aims to provide you with a comprehensive analysis of RWA, including its development history, current status and future potential.

1. RWA definition, development history and technical path

1.1 RWA Definition

RWA refers to the process of converting real-world assets (such as real estate, commodities, debt, intellectual property, etc.) into digital tokens using blockchain technology. These tokens represent the ownership or income rights of assets and can be traded and managed on the blockchain. Its core goal is to solve the problems of difficult ownership confirmation, low circulation efficiency and insufficient liquidity in traditional asset transactions through the immutability, traceability and programmability of smart contracts of blockchain.

From a technical perspective, RWA tokenization includes three key stages:

• Off-chain title confirmation : Complete asset ownership confirmation and value assessment through legal compliance procedures.

• On-chain mapping : Map asset rights to the blockchain and generate corresponding tokens.

• On-chain governance : Automated management such as profit distribution and pledge liquidation is achieved through smart contracts.

Compared with traditional asset securitization (ABS), RWA has similarities in risk isolation and cash flow restructuring, but its technological dependence requires additional evaluation of factors such as blockchain architecture, smart contract security, and cross-chain interoperability.

1.2 RWA Development History

• Early exploration (2017-2020) : The RWA concept emerged around 2017, and early projects focused on the tokenization of real estate and artworks. For example, the Securitize platform tried to put assets on the chain and explore the feasibility of tokenization.

• Institutional entry (2021-2023) : In 2021, DeFi protocols such as MakerDAO began to incorporate RWA into the ecosystem, and users can borrow and lend by mortgaging real assets. In 2023, the RWA market size reached US$5 billion, and traditional financial institutions such as Goldman Sachs and Franklin launched tokenized products, marking the entry of RWA into the mainstream vision.

• Explosive growth (2024-2025) : Traditional financial institutions such as BlackRock and Goldman Sachs are accelerating their RWA deployment, driving rapid market growth. The RWA market size has exceeded US$23 billion, becoming one of the important directions of blockchain applications.

2. Market size and growth trend

2.1 Global RWA Market Size

According to RWA.xyz, as of the end of May 2025, the total value of RWA on the global chain is about 23 billion US dollars. Among them, the TVL of the RWA protocol exceeded the 10 billion US dollar mark for the first time in March 2025, reaching about 10.4 billion US dollars on March 21. During the same period, the RWA field has grown significantly year-on-year, with a TVL growth rate of nearly 140% since the beginning of 2025. These data show that the RWA market has shown explosive growth in the past two years.

TVL of major protocols

The TVL of mainstream RWA protocols has increased significantly. For example:

MakerDAO (RWA Vaults) – The TVL of its RWA collateral vaults is approximately $1.3 billion at the beginning of 2025.

Ondo Finance – TVL is approximately $1.283 billion.

Centrifuge – TVL is approximately $441 million.

In addition, BlackRock's on-chain U.S. Treasury bond fund BUIDL has also jumped to the top with about $1.4 billion TVL, followed by MakerDAO with about $1.3 billion. These figures reflect that institutional background projects and high-quality protocols dominate the RWA field.

2.2 Growth Trends and Forecasts

Many research institutions have made predictions about the RWA market size in 2030 and given corresponding compound annual growth rate (CAGR) estimates. Boston Consulting Group (BCG) once estimated that the global asset tokenization scale could reach about $16 trillion by 2030. McKinsey and others also predicted about $2 trillion. International bank Citigroup expects the scale to be between $4 and $5 trillion in 2030, and digital asset management agency 21.co gives a wide range of $3.5 to $10 trillion. In the crypto industry, analyst Jamie Coutts pointed out that if the growth rate of about 121% in the past two years is maintained in the next five years, the RWA tokenization scale in 2030 will be about $1.3 trillion. The corresponding annual compound growth rates of the above forecasts range from tens of percentage points (1 trillion) to hundreds of percentage points (more than 10 trillion), reflecting the coexistence of RWA market potential and uncertainty. For example, growth from a few billion dollars at the end of 2023 to Coutts' estimated $1.3 trillion would correspond to an average annual growth rate of more than 120%, while reaching BCG's $16 trillion forecast would require an average annual growth rate of far more than 200%.

Key growth trends

Institutional participation is accelerating: Traditional financial giants have entered the RWA track. Taking BlackRock as an example, its Ethereum-based Treasury bond fund BUIDL was launched in 2024, and by 2025, its scale has exceeded US$2.5 billion (accounting for 41% of the global on-chain Treasury bond tokenization market share). Robinhood also submitted an RWA exchange framework plan to the SEC in 2025, and it is expected to reach US$10 billion TVL within three years. In addition, institutions such as Fidelity, Goldman Sachs, and Franklin Templeton have launched or plan to launch compliant RWA products, driving market demand.

Technological evolution drives efficiency improvement: The Ethereum ecosystem still dominates the tokenized infrastructure. As of May 2025, the tokenized assets carried by Ethereum account for about 55% of the global total. At the same time, various high-performance links and expansion solutions continue to emerge. For example, the RWA platform that Robinhood plans to build adopts a hybrid chain architecture of Solana and Base, which can achieve sub-10 microsecond matching and 30,000 TPS throughput, significantly improving settlement efficiency and reducing costs. In addition, Layer2 networks (such as Arbitrum Nova) and zero-knowledge proof technologies are being used to reduce RWA transaction costs and enhance privacy.

Regulatory policies are becoming stricter: Regulators in various countries have begun to formulate relevant rules for RWA to provide institutional guarantees for market development. Robinhood has submitted a complete proposal to the US SEC for compliance requirements such as federal licenses for tokenized assets and on-chain audits, aiming to establish standards for token issuance and trading. Regulations such as the EU Crypto-Assets Markets Act (MiCA) are also clarifying the classification and compliance standards of RWA tokens. At the same time, Hong Kong, the United States and other places have piloted allowing investors with a certain threshold to participate in RWA through compliant platforms, such as investing in government bonds and real estate through compliant stablecoins and security tokens. Overall, the maturity of policy supervision has enhanced institutional confidence and provided key support for the rapid expansion of the RWA market.

3. RWA Technical Path and Core Standards

3.1 Technical Path

The technical implementation path of RWA usually includes the following key steps and modules:

1) Asset Tokenization Workflow

• Asset selection and confirmation : clarify the value, ownership boundaries and transferability of off-chain assets;

• Legality audit and SPV establishment : Asset custody through a custodian institution or the establishment of a special purpose vehicle (SPV);

• Token Minting : Generate corresponding tokens according to standards such as ERC-20, ERC-721 or ERC-3643;

• Off-chain data access (Oracle/IOT) : Update asset status in real time through oracles, IoT or third-party audits;

• Value guarantee mechanism : Maintain the anchoring relationship between tokens and real assets through custody, insurance, excess mortgage, etc.

2) RWA Protocol Stack

3.2 Core Standards and Tools

• ERC-3643 (T-REX) : One of the most mature RWA token standards, supporting identity whitelisting, regulatory control, and permission management;

• ERC-1400 : A compliance framework for security tokens that supports modular regulatory compliance design;

• Chainlink / Pyth Oracles : Provides trusted synchronization of off-chain data such as prices and asset status;

• Multi-signature/custodial tools : such as Gnosis Safe, Anchorage Custody, etc., to ensure asset security and governance compliance;

• TEE (Trusted Execution Environment) : Ensures that sensitive off-chain data can still run privately and securely during on-chain interactions.

RWA's vision is to introduce tens of trillions of dollars of real assets into the on-chain financial system, unleash its liquidity and composability, and build a new generation of more efficient, transparent, and inclusive financial infrastructure. Its technical path must not only solve the dual problems of "on-chain programmability" and "off-chain trusted connection", but also take into account legal compliance, audit mechanisms, system security, and market participation paths.

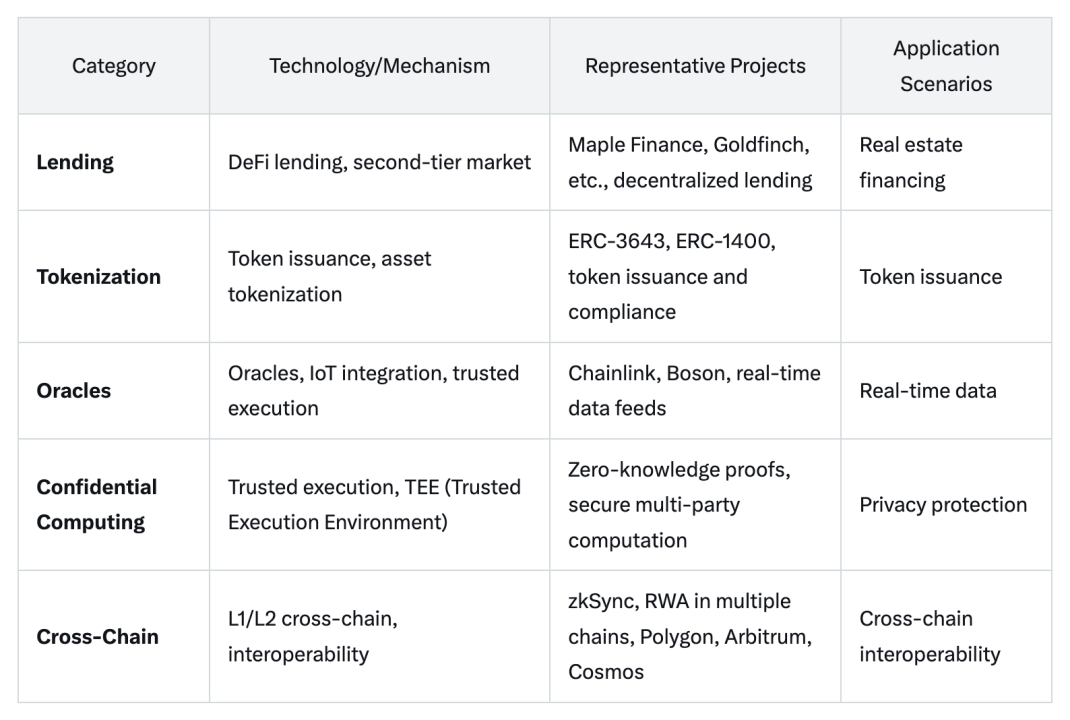

4. Typical RWA asset categories and practical applications

4.1 Typical RWA asset types

The paths for real assets to be put on the blockchain are becoming more diversified. The mainstream RWA projects are centered around the following types of assets, relying on the credit and income structure of real assets to achieve tokenized mapping. Such assets can be roughly divided into the following four categories:

1. Debt assets (real-world securities)

Such RWA projects are usually linked to real-world debt instruments (such as U.S. Treasury bonds, corporate bonds, accounts receivable, etc.) and represent one of the most mature and mainstream tracks, with high transparency, strong compliance attributes and predictable returns.

Typical projects:

• Ondo Finance : uses U.S. Treasury ETF as underlying assets and issues tokens such as OUSG.

• Maple Finance : Connecting real-world credit demanders with DeFi liquidity providers through structured credit products.

• Centrifuge : Put assets such as accounts receivable and invoices on the chain and connect to the Tinlake protocol for lending.

2. Real estate assets (real estate, etc.)

Through real estate valuation and rental income, real estate assets can be split into tradable tokens for DeFi staking or asset allocation, with good asset security and cash flow foundation.

Typical projects:

• RealT : Provides tokenized holdings based on U.S. real estate, and token holders can obtain rental income.

• Propy : Real estate transactions and property registration are put on the chain to make the home buying process transparent.

• Lofty : A fragmented real estate investment platform that supports proportional dividends and asset management.

3. Commodity assets (gold, carbon credits, oil, etc.)

Through the support of real goods or certificates, tokens linked to their value are issued for storage, risk hedging or transaction circulation.

Typical projects:

○ PAXG : A gold-backed stablecoin issued by Paxos. Each token corresponds to a certain amount of physical gold.

○ OpenCarbon : A carbon credit tokenization platform that puts carbon emission reduction certificates on the chain.

○ Tangible : Tokenize physical assets such as wine and watches for trading and storage.

4. Other real-world asset categories (copyright, insurance, invoices, intellectual property, etc.)

This is an innovative field in the early stages of RWA exploration, representing assets with weak liquidity but strong innovation, and is suitable for incubation on specific vertical platforms.

Typical projects:

• Re : Insurance risk exposure tokenization platform, providing on-chain reinsurance for DeFi.

• IP3 / Story Protocol : Exploring solutions to put the value of intellectual property on the chain.

• Goldfinch : A credit lending platform that supports small and micro loans in developing markets.

4.2 Practical Application of RWA

(1) Investment-oriented RWA: Return anchoring of virtual assets

The practice of investment-oriented RWA can be traced back to the exploration of the stability mechanism of the DeFi ecosystem. Its typical model is to use the income of real assets to provide value support for virtual assets. This "asset endorsement" logic has already taken shape in the early practice of MakerDAO. The protocol builds a decentralized value foundation for its stablecoin DAI by accepting real assets (such as US Treasury bonds) as collateral. With the entry of traditional financial institutions, this model has gradually evolved into a more mature institutional-level solution. Take the BUIDL fund issued by BlackRock as an example. This product tokenizes fund shares through the Ethereum network and allocates the raised funds to short-term US Treasury bonds, so that token holders can obtain Treasury bond returns in real time.

The core features of this type of RWA are reflected in three aspects:

First, the underlying assets are concentrated in highly liquid traditional financial instruments (government bonds, money market instruments, etc.);

Second, the initiators are mostly licensed financial institutions or compliant DeFi protocols;

Third, the operational goal is to enhance the stability and attractiveness of the virtual asset system through real asset returns. From a regulatory perspective, this type of application essentially builds a transmission mechanism of "traditional asset returns-on-chain token distribution", and its compliance focus is to ensure the security of underlying asset custody, the transparency of income distribution, and the compliance of cross-border capital flows.

(2) Financing-oriented RWA: Liquidity liberation of traditional assets

Financing-oriented RWA presents a completely different value logic - its essence is to create a new financing channel for low-liquidity assets through blockchain technology. The green energy financing case in the Ensemble sandbox of the Hong Kong Monetary Authority belongs to this category. ([Note 1]) The project party tokenizes the income rights of mainland new energy power stations by building a cross-chain bridge to attract foreign capital to participate in investment.

This type of RWA is innovative in three aspects:

First, the underlying assets are expanded to include non-standard assets (such as infrastructure and commercial real estate), lowering the investment threshold through segmentation;

Secondly, the transaction structure design places more emphasis on cash flow restructuring and risk isolation, with a common SPV (special purpose vehicle) and token holders’ rights and interests being layered;

Finally, smart contracts are deeply embedded in the entire asset operation process to realize the automated execution of functions such as rent distribution and performance guarantee. From the perspective of regulatory adaptability, such applications need to pay special attention to the reliability of the underlying asset valuation method (especially for unlisted assets), the resolution mechanism of cross-border legal conflicts (such as the choice of applicable law for property rights), and the applicability of public offering clauses under the securities law (depending on the economic substance of the token). The uniqueness of Hong Kong's regulatory framework lies in that it allows professional investors to participate in such innovative projects through private placement channels, while maintaining a cautious open attitude towards mass market participation through the sandbox mechanism.

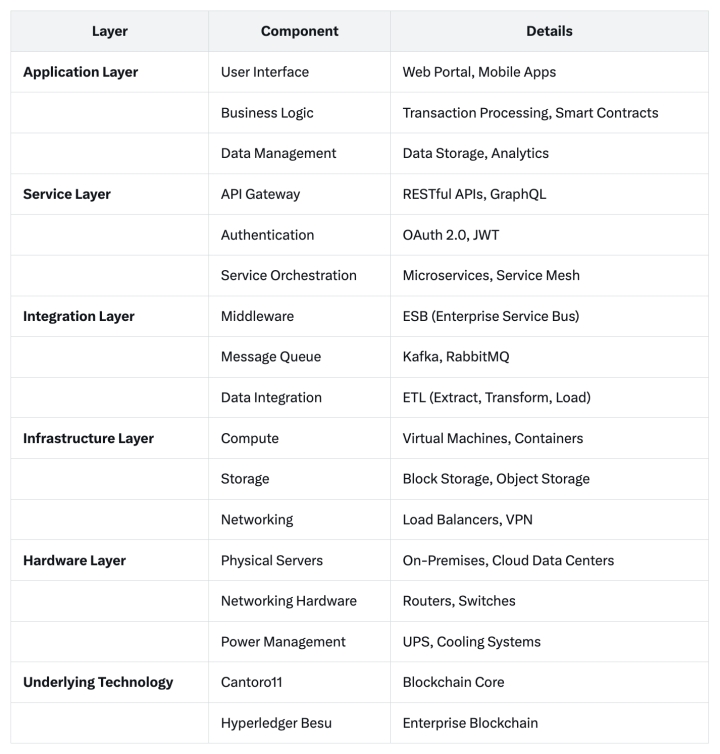

4.3 RWA Practical Issuance Process

The following figure shows an example of the digital platform architecture in the Evergreen digital bond project and the overall project structure of a general RWA:

*The overall architecture of the digital platform used by the Evergreen project ([Note 2])

*General RWA project structure summarized based on practical experience and public information

5. Development status and representative projects of global, China, US and Hong Kong markets

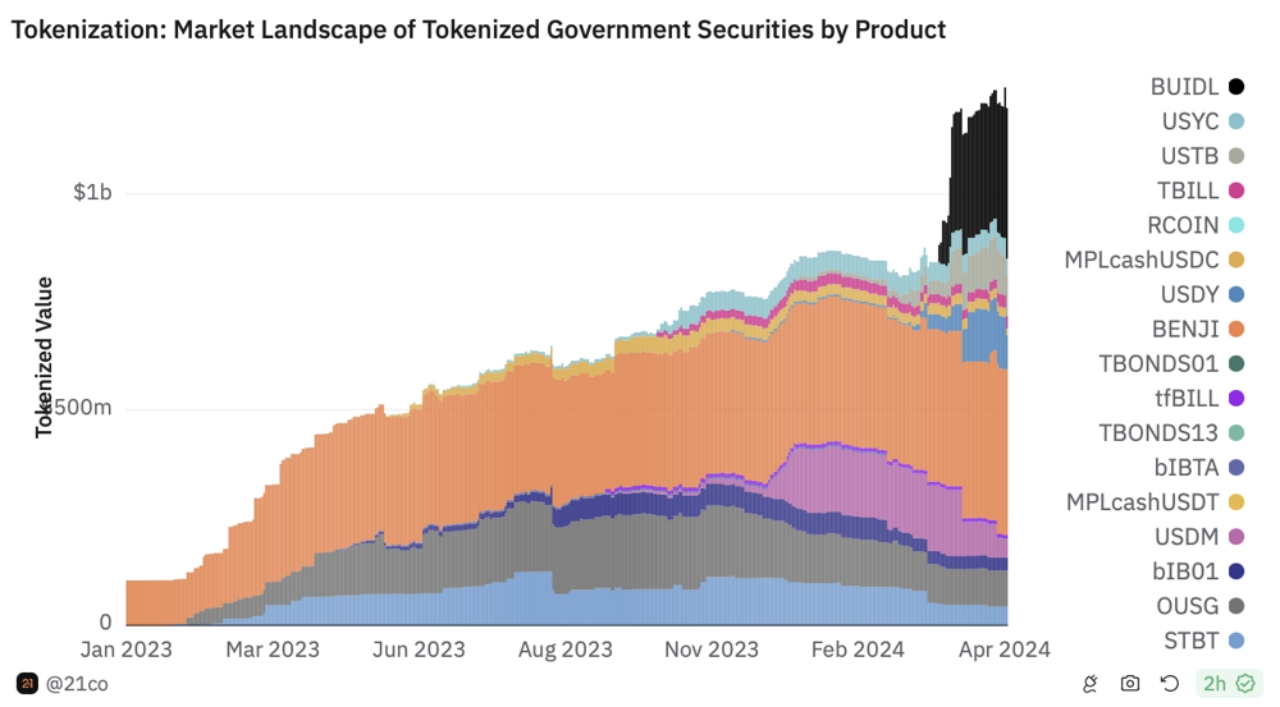

At present, the global RWA market is growing rapidly. According to data, as of May 2024, the RWA market size exceeds US$22 billion and is still growing. Among them, developed markets represented by the United States and innovative platforms focusing on blockchain have led this trend. For example, institutions such as Ondo Finance, Franklin Templeton, and Securitize in the United States have issued bonds and fund tokens based on public chains such as Ethereum; DeFi platforms such as MakerDAO, TrueFi, and Goldfinch have promoted private lending and on-chain lending; the RWA categories with the largest market value are government securities and fixed income, and the issuance volume of some projects has exceeded billions of dollars.

As shown in the figure above, the scale of the tokenized government securities market (such as on-chain U.S. bonds, treasury bonds, government fund shares, etc.) has risen rapidly since 2023 and has now exceeded US$1 billion. This trend reflects the continued interest of institutional investors in RWA. Well-known asset management giants have entered this field: BlackRock has issued a total of US$260 million in RWA funds on Ethereum, and Citi, JP Morgan, Goldman Sachs, etc. have also issued securities or private equity funds on the test chain. Leaders in the DeFi field (such as Maker and Aave) are more concerned with using RWA as collateral for lending.

In the Chinese market, due to the strict regulatory restrictions on the issuance of crypto assets, RWA applications are more developed from the perspective of technology and industrial chain. In 2024, there were several pilot projects for energy and equipment assets on the chain in China . For example, Shanghai Shutu Blockchain Research Institute and Ant Digital Technology "packaged" about 4,000 battery swap cabinets operated by Anhui Xunying New Energy Group on the chain, raised funds through private placement, and provided financing for green energy infrastructure; the charging pile project of Langxin Group and Ant Digital Technology completed nearly 100 million yuan of RWA financing in August 2024 (with more than 9,000 charging piles as the target). The "AntChain Inside" technical solution proposed by Ant Digital Technology has been applied in the field of charging, swapping, photovoltaic and other physical assets on the chain. In addition, China Academy of Information and Communications Technology took the lead in drafting the first RWA on-chain technical specification in 2025 to promote the standardization of physical assets on the chain. Although there is no large-scale public RWA transaction in China at present, the above-mentioned energy and equipment asset on-chain projects have explored a model for domestic RWA. It is worth noting that Hong Kong is also actively promoting the implementation of RWA: the Hong Kong Monetary Authority launched the "Ensemble Project Sandbox" in 2024, covering tokenization scenarios such as fixed income, funds, green finance, and supply chain financing; at the same time, Hong Kong Victory Securities served as the custodian of the first Shanghai TreeGraph Blockchain RWA project, indicating that Hong Kong regulators support compliant custody services.

The figure below illustrates the distribution of the main participants in the current RWA tokenization ecosystem, including asset issuance platforms, trading distributors, DeFi protocols, custodians, on-chain networks and data services, etc. It can be seen that the RWA ecosystem connects financial institutions and blockchain platforms, such as issuers (Tokeny, ADDX), DeFi platforms (MakerDAO, TrueFi, Centrifuge, etc.), custodial wallets (Fireblocks, MetaMask, etc.) and specialized service providers (Chainlink oracle, Inveniam data authentication), etc., jointly build the infrastructure.

In general, the global RWA field includes both CeFi projects involving traditional financial giants and DeFi projects attempting decentralized finance . The regulatory environment in markets such as Europe and the United States is relatively mature, which has promoted large-scale compliance pilots; China and Hong Kong are more focused on the application practice of green energy and infrastructure assets on the chain.

VI. Regulatory attitudes and compliance policies in various regions

6.1 Hong Kong’s regulatory policy: from pilot innovation to dual-track supervision

6.1.1 Evolution of the regulatory framework for security tokens (STOs) and tokenized securities

As early as March 2019, the Hong Kong Securities and Futures Commission (SFC) issued a "Statement on the Issuance of Security Tokens", which clearly stated that most STOs are likely to fall into the category of "securities" under the Securities and Futures Ordinance (SFO) and must comply with all applicable provisions of the securities law. Unless exempted, any individual or institution that promotes, sells or trades STOs in Hong Kong or to Hong Kong investors must hold a Type 1 regulated activity license issued by the SFC.

Since then, with the development of tokenization technology, the China Securities Regulatory Commission issued the "Circular on Intermediaries Engaged in Tokenized Securities-Related Activities" (hereinafter referred to as the "Circular") in November 2023, further building a dual-track regulatory system with " underlying financial asset attributes as the main and technical supervision as the supplement ", focusing on the following aspects:

6.1.2 Core regulatory logic and technical compliance requirements

• Definition: Tokenized securities refer to financial instruments that are issued or traded using distributed ledger technology (DLT), but whose underlying nature is traditional securities (such as bonds, funds, etc.).

• Regulatory application logic : It is still managed according to the SFO, while adding technical regulatory requirements such as information disclosure, security, settlement, governance, etc. for the DLT architecture, emphasizing "technology neutrality and risk sensitivity".

6.1.3 Core regulatory points

6.1.4 Summary of the characteristics of Hong Kong RWA supervision

• Mature legal basis : If RWA is essentially a security or fund, it is already covered by existing laws and there is no need to create a new legal scope;

• Supervision focuses on technical compliance : separate governance for DLT application risks;

• Policies are gradually opening up : the original restrictive policies (such as only professional investors) have been relaxed, reflecting the policy's inclusiveness of innovation.

6.2 US Regulatory Policy: Functional Testing and Judicial Case Dominance

6.2.1 SEC’s regulatory position on digital assets and RWA

The core attitude of the U.S. Securities and Exchange Commission (SEC) on the regulation of RWA and tokenized assets can be summarized as: " Whether it constitutes a security depends on the substantive analysis of the Howey Test ." The SEC determines whether it falls within the scope of securities regulation through the following dimensions:

• Does investing involve investing money?

• Are you dependent on the efforts of others to achieve your expected benefits?

• Is there a common enterprise involved in the investment?

• Do investors expect profits?

6.2.2 Regulatory Characteristics of the US in the RWA Field

6.2.3 Challenges of RWA Regulation in the United States

• Legal gaps and regulatory gray areas : There is no federal unified digital asset bill so far, and the market relies more on case law and administrative interpretation;

• The compliance path is complicated : different investor categories, transaction links, and on-chain and off-chain structures must all match specific compliance requirements;

• Insufficient international regulatory coordination : There are conflicts with the EU MiCA, Hong Kong SFO, etc., making cross-border RWA products difficult to implement.

6.3 Dubai

Dubai regulators actively support RWA tokenization innovation and have established a relatively clear regulatory framework. The main institutions are the Dubai Virtual Asset Regulatory Authority (VARA) and the Dubai Financial Services Authority (DFSA) . On May 19, 2025, VARA updated the "Virtual Asset Issuance Rulebook", explicitly incorporating RWA token terms, and authorizing regulated exchanges and brokers to issue, distribute and list such tokens. The new rules classify RWA tokens as "asset-referenced virtual assets (ARVA)", defined as tokens that represent direct or indirect ownership of real assets and bring income rights or stable value, requiring issuers to hold a type of virtual asset issuance license and provide a complete white paper and risk disclosure statement. DFSA launched the "Tokenization Regulatory Sandbox" on March 17, 2025, allowing companies to test tokenized securities and RWA projects in the controlled environment of the Dubai International Financial Center. DFSA sandbox participants include tokenized investments and RWA projects such as stocks, bonds, Islamic bonds, and collective fund units; pure cryptocurrency and fiat stablecoin projects are not within the scope of this plan. The DFSA provides regulatory exemptions for sandbox members, including conditional relaxation of some prudential and capital requirements during the testing phase, thereby lowering the threshold for innovation. As of April 24, 2025, the first round of applications has ended, and selected companies in the future will need to obtain the corresponding DFSA license before they can officially operate.

• Regulators and regulations: Dubai has dual-track supervision through VARA (for the UAE) and DFSA (for the DIFC financial free zone): VARA's 2025 rulebook clarifies the ARVA concept and issuance requirements; DFSA launched the Tokenisation Sandbox after several industry meetings in 2024-2025. The federal constitution and local laws give DIFC and VARA independent powers equivalent to international standards, making Dubai's regulatory framework internationally equivalent to the EU.

• Asset categories and token nature: Dubai's regulatory system covers the tokenization of RWA and traditional securities extensively. The VARA rules include RWA tokens in the ARVA category, allowing all types of real assets (including real estate, commodities, financial assets, etc.) to be traded in tokenized form. The DFSA sandbox is open to both tokenized securities and physical asset projects, and participating institutions only need to have the corresponding licenses or testing qualifications. It should be noted that Dubai regulation explicitly excludes pure crypto tokens and fiat stablecoin projects to highlight support for real asset investments. In general, as long as regulatory requirements are met, RWA tokens can be circulated in regulated markets.

• Technological risks and investor protection: Dubai's regulatory focus is on license management and information disclosure. VARA requires issuers to obtain a type of virtual asset issuance license and disclose risks; DFSA stipulates that participating companies must have a deep understanding of relevant laws and regulations and have products or services available for testing. Issuers and exchanges must fulfill their full risk disclosure obligations to ensure that investors are informed. Under the sandbox system, the DFSA may conditionally relax regulatory requirements, but only on the premise of maintaining confidence in the integrity of the financial market. Overall, Dubai's regulatory environment is open and prudent, providing support for innovation through license control and sandbox experiments, while emphasizing compliance operations to prevent technological and market risks.

6.4 Comparison of RWA regulatory environments in different regions

Summary points:

1. Hong Kong : It adopts a dual-track regulatory model of "asset attributes as the main and technical supervision as the auxiliary". The legal basis is mature and the policies are gradually relaxed, which is conducive to the implementation and innovation of compliant RWA projects.

2. United States : The functional regulatory model based on the Howey Test creates significant uncertainty, complicated compliance paths, fragmented regulation, and makes it difficult to form a unified market.

3. Dubai : It has established clear rules and innovative mechanisms (such as sandbox) through the VARA+DFSA dual-track system , and supports RWA. It is one of the regions with the most "aggressive and feasible" supervision.

VII. Future Prospects and Potential Forecast

RWA is widely regarded as the "golden key" connecting traditional finance and blockchain in the Web3 field, and has great prospects for future development. According to industry reports, the global tokenized asset market size will reach about 16 trillion US dollars by 2030, equivalent to about 10% of the global GDP. The following trends are expected to emerge in the next few years:

1. More institutional capital is entering the market: Traditional financial giants such as JPMorgan Chase, HSBC, BlackRock, and Goldman Sachs are accelerating their deployment of RWA, and more banks and asset management companies are expected to issue or invest in on-chain assets. For example, JPMorgan has been developing digital securities technology internally, and BlackRock's large funds have been issued on the public chain. In the future, large institutional funds may operate in a blockchain manner, driving the rapid expansion of on-chain assets.

2. Expansion and diversification of asset types: In addition to existing bonds, real estate, and commodity RWAs, more traditional assets (such as stock equity, infrastructure income rights, intellectual property rights, etc.) will be included in the tokenization. Combined with digital twin (Digital Twin) and oracle technology, more real-time data-driven assets can be put on the chain in the future, such as real-time data contract derivatives, carbon credit dynamic trading, etc.

3. Technology and standard upgrade: As asset security and compliance requirements increase, more standard protocols for RWA (such as the ERC-3643 security token standard) will emerge in technology to support richer permission management and compliance tools. In addition, cross-chain interoperability protocols (such as IBC, XCMP) and trusted hardware/zero-knowledge proof technologies will improve the circulation efficiency and privacy protection of RWA.

4. Improved regulatory system: Regulators around the world have begun to formulate targeted policies, and may issue a unified framework or guidelines in the future. For example, the EU MiCA has mentioned the classification of RWA assets, and the US SEC is also considering the registration path for digital securities. As experience accumulates, regulatory requirements for RWA will become clearer, providing compliance guidance for projects, and regulatory technology (RegTech) will also be used to monitor the compliance status of on-chain assets in real time.

5. Integration of green finance and innovation: Green assets (such as renewable energy and carbon reduction) will become a hot spot for RWA. Hong Kong and other places already have tokenized sandboxes specifically supporting green finance. It is expected that RWA will be deeply integrated with sustainable development goals to provide enterprises with innovative financing channels.

In short, RWA is expected to attract more traditional investors to enter the crypto market by lowering the investment threshold and improving liquidity, while injecting vitality into the financing of the real economy. Driven by the gradual improvement of compliance technology and market mechanisms, RWA will become an important growth pole for the Web3 industry in the future. With the deep integration of public chains and traditional finance, the RWA market is expected to form a trillion-dollar scale, ushering in a new era of digital finance.

All Comments